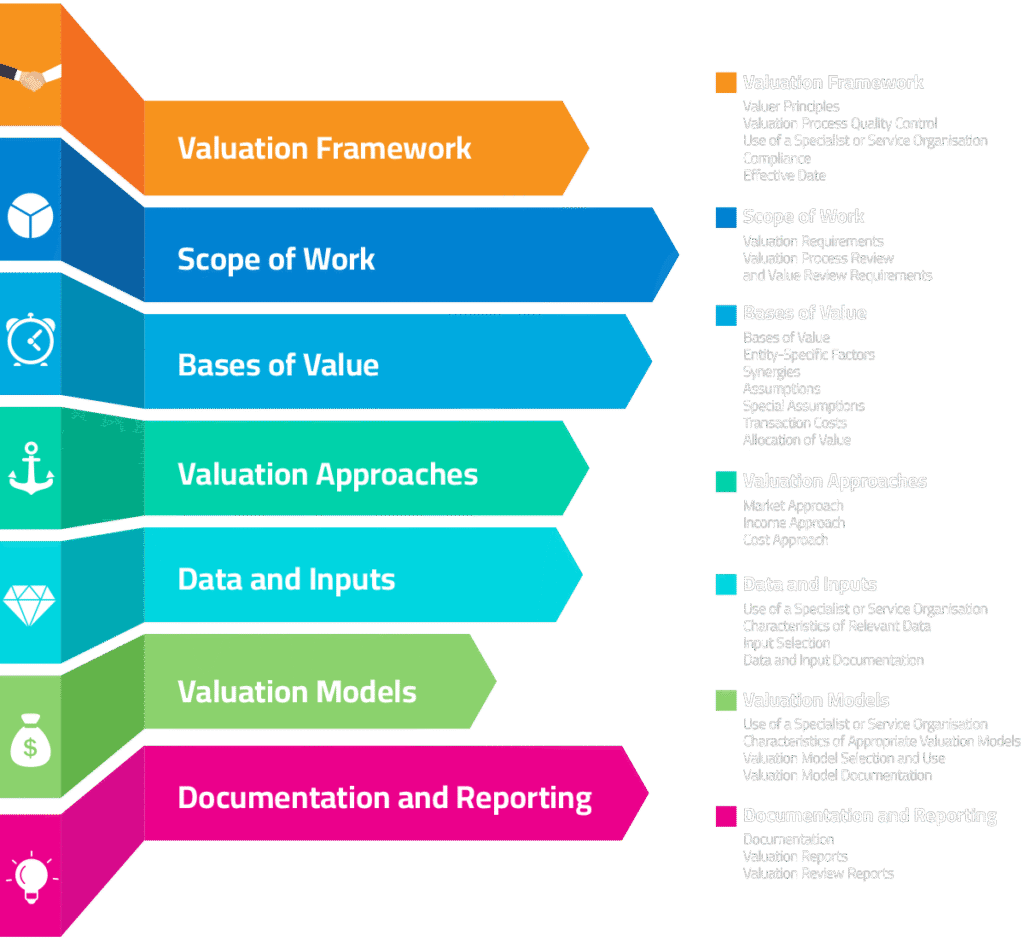

Valuation Framework

- The extent of the controls should be determined having regard to the intended use, intended user, the asset and/or liability being valued and the complexity of the

- The controls should assess the judgements made during the valuation including their reasonableness and freedom from bias in determining the value.

- The controls should be The documentation should contain sufficient detail to allow another valuer, applying professional judgement, to understand the effectiveness of the controls.

- There should be periodic assessment of the controls to ensure that their integrity and completeness are appropriate as of the valuation date. The periodic assessment should be

- If the valuer is able to address valuation risk they may then perform monitoring procedures with respect to their own compliance and control policies and

- The valuer should conclude that the level of valuation risk, subject to controls in place, is appropriate given the intended use, intended user, the characteristics of the asset or liability being valued and the complexity of the valuation.

- Use of Specialist or Service Organisation

- If the valuer does not possess the necessary technical skills, experience, data or knowledge to perform all aspects of a valuation, it is acceptable for the valuer to seek assistance from a specialist or service organisation, providing this is agreed and

- Prior to using a specialist or service organisation the valuer must assess and document the knowledge, skill and ability of the specialist or service organisation. Relevant factors include but are not limited to:

- experience in the type of work performed,

- professional certification, licence, or professional accreditation of the

specialist or service organisation in the relevant field,

- reputation and standing of the specialist or service organisation in the particular

- When a specialist or service organisation is used, the valuer must obtain an understanding of the process and findings to establish a reasonable basis to rely on their work based on the valuer’s professional judgment.

- Compliance

- In order to be IVS compliant, the valuation must meet the requirements of the General Standards, the Appendices, as well as Asset Standards, if

- consist of mandatory requirements that must be followed in order to state that a valuation was performed in compliance.

Valuer Principles

- Ethics

The valuer must follow the ethical principles of integrity, objectivity, impartiality, confidentiality, competence, and professionalism to provide a non-biased valuation and to promote and preserve the public trust.

- Competency

The valuer must have the technical skills, knowledge and experience required to appropriately complete a valuation.

- Compliance

The valuer must disclose or report that IVS were used for the valuation and that they complied with those standards in performing the valuation.

- Professional scepticism

The valuer must apply an appropriate level of professional scepticism at every stage of the valuation.

- Valuation Process Quality Control

- There must be valuation process quality controls (“the controls”) around the valuation

- The controls help ensure that valuations are performed objectively, transparently, without bias and in compliance.